The Reports of Oil’s Death Are Not Greatly Exaggerated

The oil industry was having a very bad year before the COVID-19 lockdown made things worse. Green Parliamentary Leader Elizabeth May’s observation that oil is dead could be, based on a preponderance of evidence, more than just wishful thinking.

Elizabeth May

May 7, 2020

When I pronounced during a news conference in Ottawa on Wednesday that “Oil is dead,” I expected neither surprise nor outrage. I thought I was just pointing out the glaringly obvious.

Of course, our dependency on fossil fuels has not ended; it hasn’t yet become an economic casualty of the COVID-19 pandemic. But fossil fuels are assuredly — in Canada and around the world — an endangered commodity. And Canadian oil in particular will be, for the long term, a product lacking investors.

Years before the pandemic hit, major oil giants started leaving the oil sands. Many actually pointed to the fact that bitumen was the most carbon-intensive oil in their asset base. They talked about wanting to avoid being stuck with unburnable carbon; “stranded assets.” Royal Dutch Shell, Total SA, Statoil (now Equinor), Conoco Philips, Imperial Oil, Marathon Oil, Exxon Mobil and, even Koch Industries had pulled out.

If you follow the money, what was going on?

The bitumen produced in the Alberta oil sands is both very expensive to produce and of inherently low value. To be profitable it takes two things — government subsidies and a price of $70 a barrel. Canada’s subsidies to get the oil sands in business started in earnest in the mid-1990s when oil was selling for less than $30 a barrel. Without billions of federal dollars (primarily delivered as generous Accelerated Capital Cost Allowances from the feds, and the world’s lowest royalty rates from the province) the oil sands would not have moved beyond half a million barrels a day (mbd). Today, they are approaching 3 mbd. And even at their height, oil sands contributed less than 3 percent to Canada’s GDP.

As the price of oil plunged, so did investment. Teck had relied on oil prices of more than $80 barrel in its environmental review for the Frontier Mine project near Fort McMurray. As oil prices dropped, the potential for profitability withered, and Teck withdrew its application for the Frontier Mine. The accompanying statement from Teck CEO Don Lindsay was memorable for its forthrightness about the role climate change played in the decision. “The promise of Canada’s potential will not be realized until governments can reach agreement around how climate policy considerations will be addressed in the context of future responsible energy sector development,” Lindsay wrote in a letter to the federal environment minister published February 23. “Without clarity on this critical question, the situation that has faced Frontier will be faced by future projects and it will be very difficult to attract future investment, either domestic or foreign.”

And that was before Saudi and Russian collusion to really open the taps and flood world markets with cheap oil. The main target of their action was U.S. unconventional oil — Bakkan shale. It is the shale plays that gave the U.S. unprecedented energy security. But like Canadian bitumen, shale is very expensive to produce. It is essentially fracking for oil. By flooding the market, the OPEC-Russian play was to knock out the more expensive competition.

Eric Reguly wrote in the Globe and Mail on March 31: “By this week, West Texas Intermediate, the U.S. benchmark, was trading at about US$20 a barrel, down from its 12-month high of US$66. The price of some minor grades of U.S. crude, such as the thick oil used to pave roads, actually turned negative, meaning the producer was paying the buyer to cart the guck away,” adding that the strategy of the shale guys of ramping up production by record amounts until the United States surpassed Saudi Arabia and Russia to become the world’s top oil producer was bound to backfire (Canada’s rising output from the oil sands also helped to flood the market). “The triggers were the pandemic and the decision by Saudi Arabia and Russia to pump like mad to intensify the shale industry’s pain. If they hand a life jacket to the shale boys, it will be made of concrete.” As will be any life jacket for the oil sands.

Canada’s bitumen is still a product of low value. Whether at “tidewater” or moving in pipelines to the U.S., on arrival it must be separated from the diluent with which it was mixed to allow a solid lump to flow, and then go through an expensive upgrading process in order to be refined. In a world awash in cheap refinable oil, Canadian bitumen was being priced out of the market. But then the future of oil globally got even more wobbly. Over the past few weeks, it seems every day a new report comes out that makes it clearer that fossil fuels are done.

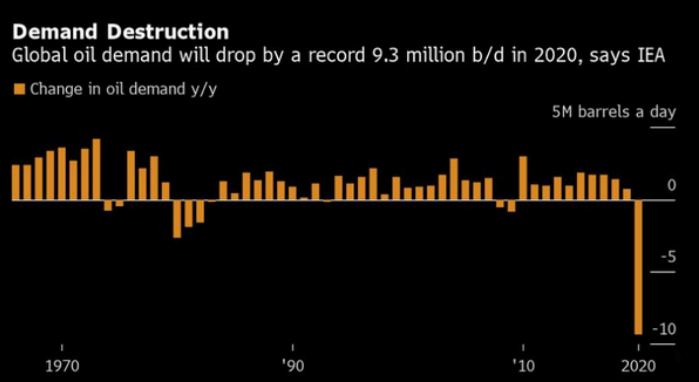

The International Energy Agency in its Oil Market Report for April said that if the pandemic continues to spread globally, global oil demand could fall by a record 9.3 mbd in 2020. CNN reported on April 29th that “the oil industry is bracing for the effects of the crisis to linger.” This week, the IEA Global Energy Review predicted that “Energy demand will never be the same,” per the Forbes headline. The only energy product in demand is renewable energy, which will grow 5 percent in 2020 to produce 30 percent of the world’s electricity by year end.

It is debatable how long demand will stay low, but there is no doubt that the shock to the energy world is profound, and coupled with the imperative of meeting Paris commitments and the pressure from people accustomed to clear skies during the lockdown, governments around the world are going to bank on future energy winners, not a polluting legacy of the past.

On Tuesday, a major study was released by the Oxford Review of Economic Policy, with lead authors, Nobel Prize winning economist Joseph Stiglitz and former Chancellor of the Exchequer Sir Nicholas Stern, advising that in re-starting the world economy after the pandemic, investments going to renewable energy and energy efficiency were the right moves for the economy. Trying to support fossil fuels would be far less effective.

As Sir Nicholas had warned last week at the Petersberg Climate Dialogue, a major global discussion among 30 governments, investing in the fossil fuel sector for job creation was short-sighted. “The jobs of the past are insecure jobs,” he said. “[To create future jobs] we need the right kind of finance in the right place at the right scale at the right price.” And two days ago, Royal Dutch Shell CFO Jessica Uhl warned investors of “ …major demand destruction that we don’t even know will come back,” during the company’s latest earnings call.

When the establishment energy agencies, top economists and multiple governments — and even the executives of major fossil fuels companies — speculate that oil will never bounce back, and that of all global oil, the weakest market case is for Canadian bitumen, I was only saying, in announcing the demise of oil, something that needed saying.

The irony is that we always thought the death of oil would be due to an exhaustion of supply. But it is, it seems, a drop in demand that has hastened the industry’s obsolescence. More than a century ago, whale oil ceased to be the way people lit their homes, not because the industry killed all the whales but because – kerosene- wiped out demand for the product.

The combined impacts of the world glut of cheap oil, low demand and the arrival of disruptive innovation in the form of renewable energy will not end our use of oil overnight.

But the world is not the same as it was last year, or even months ago. Oil, as the energy of the future, is dead.

Policy magazine Contributing Writer Elizabeth May, MP, is leader of the Green Parliamentary Caucus.